The stock market has been sluggish in recent weeks: the indexes are close to the lows of 2017 and 2018. The frightening news cycle and frenzied financial professionals believe that the stock market may fall even lower. Recent data and business closures demonstrate that a greater recession is possible. I believe that this recession, or the fear of such a recession, is positive for the U.S. economy. Let us not forget that we have already seen signs of life, in every economic recovery, to be greatly disappointed. No matter where the short-term equity market goes, the long-term strategy will always be effective. Two years from now, the stock market may still decline by 30%, but 20 years from now, the market will historically yield at least 10%.

As you probably know, research shows that professional investors have difficulty outperforming the market with stock selection. But as with any statistical data, be cautious about academic topics that have selected bias. Most of these data refer to professional investors as any person who can open a fund. Many well-connected or trust fund babies like Chelsea Clinton’s husband (Marc Mezvinsky) always underperform the market. Pension and endowment funds received 80 cents for every $1 invested by Marc Mezvinsky. Most of these professionals are rich enough to use their capital or well enough connected to collect money from close networks. These affluent and connected professional groups rarely perform the required investment due diligence. Buffet famously said, “Wall Street is the only place that people ride to in a Rolls Royce to get advice from those who take the subway.”

Losing out on other opportunities

In this regard, there are many hidden costs to stock-picking. For example, in 2017 more retail investors bought REIT stocks because it was an outperforming the index average. The Real Estate Investment Trusts (REITs) were the best performing industry from 2010 to 2017,the entire industry quickly turned into one of the worst investment opportunities during and after the crash. Malls were a major industry to buy between the 1970s and late 1990s; most developers focus their efforts to build out malls that are quickly becoming empty shells and debt load. If you didn’t know much of this real estate information before reading this post, then you are one of these stock pickers that are at risk of losing money.

Nevertheless, too many people consider themselves a stock-picking genius. The majority of people will be smart enough to invest, but being smart does not offset a higher return. Being a business-orientated or entrepreneurial individual doesn’t make you more qualified as an investor either. Being an investor is a profession, such as being a firefighter. If your house is on fire, the least qualified person to save your house from fire – it’s you. Anyone can learn about fire safety, but that doesn’t mean they have the knowledge to use that information to save themselves from a fire.

Many people are unwilling to apply due diligence to investments. Anybody can outperform for a few years in a bullish time. The common characteristics of retail stock pickers are individuals who lack financial skills, often have short-term benefits in their portfolio, and lack of long-term stocks.

The Investment Hidden Fees

What are the other hidden fees of stock picking? I called it the T&T problems Time & Taxes

The first cost is Time. If you have little knowledge and try to spend time learning, then you are racing against the clock against someone that is simply more knowledgeable and prepared. Novice investors spend time choosing stocks and never learn more about their investment through due diligence. Studying makes you informative, but it’s a long process before you get really knowledgeable to execute an investment. Knowledge originates primarily from information and experience. Everyone on the internet is informed about politics, but not everyone is knowledgeable. If TV ran the news on Biology and Chemistry 24/7, like political news, we would all feel like we can discuss science topics like we are all Ph.D. Scientists. I have another blog which is going to talk about the difference of being informed and knowledgeable. If you continue to choose stocks without being fully informed, you will underperform the market by 5% or more per year (50% in potential missed earnings over 10 years)

The second cost is Tax, if you’re trading in a taxable account. The gap between short- and long-term capital gains is significant. When trading shares, it may be tempting to exit positions, particularly well after just a few months. Trading often leads to greater tax costs and I avoid it. Capital tax gain taxes are 0 to 20% vs income taxes that can be about 25% to 40%. Consider the amount of money you will leave on the table if you pay income tax on your investment performance. My investment strategy is to target long term positions over short term capital gains. Most people are thrilled to receive short-term profit (but they don’t realize that they pay income taxes on it).

Time & Taxes

Taxes and time can seriously erode performance, particularly for high-frequency stock traders in higher tax brackets. Most economic research studies show these and other mistakes made by the ordinary investor can reduce returns by 4% or more a year relative to a stock index (which hasn’t included the short-term tax fees).

It’s important to understand that there are two main approaches to investing in the stock market. The first is passive investing, which aims to achieve the average market return of around 7-8%.

The other approach is to invest in individual stocks with the goal of outperforming the S&P 500. This approach requires more time and effort, as it involves researching and selecting specific stocks rather than just investing in a broad index. If you have any specific questions or need clarification on anything mentioned in this post, feel free to reach out to me at TomNguyen@agarwoodcapital.com.

1. Decide if you want to put in the time to beat the stock market average returns (Week 1)

Passive investing- The goal of passive investing is to achieve average stock market returns, which are estimated to be around 7% to 8% over the last 100 years. To start passive investing, it is recommended to buy a mutual fund or ETF that represents the S&P 500. This can be done through robo-advisors or standard investment advisors, who provide these mutual funds and ETFs.

Robo-Advisor Services

When choosing a service for passive investing, it is important to go with low-cost options such as Vanguard or Fidelity, or robo-advisors like Wealthfront or Betterment. Management costs should be below 1% of your total asset value.

A note about indexes: It is also important to note that different indexes represent different segments of the market. The S&P 500 represents the 500 largest companies in the US, and is therefore often used as a benchmark for the overall performance of the US stock market. Other indexes, such as the Dow Jones (DJI), only include a small number of companies and may not be representative of the broader market. This is why the S&P 500 is considered the standard benchmark instead of other indexes.

Active investing- The goal of active investing is to pick stocks and outperform the stock market average, which is represented by the S&P 500. Active investing requires putting in the time to research and analyze both individual stocks and the overall market. If you choose to become an active investor (or the DIY approach, as I like to call it), you will need to learn key aspects for analyzing a stock and strategies for ending the year with returns above the stock market average.

Learning about an industry, company, and competitors

Learning about investment strategies can outperform the average return

Learning how to read and create financial statements

If becoming an active investor is the path you want, then continue reading.

2. Start by reading about industries and companies that are the most familiar to you. (Week 2)

It’s important to choose a business industry that is easy for you to comprehend, as this will make your investment journey more enjoyable and successful. One way to do this is to select an industry that is related to your profession or one that you have experience with through your regular purchases.

For example, if you work in the apparel industry, you may find it easier to understand the operations of an apparel company. The apparel industry is a multi-billion dollar investment opportunity, but it can also be highly competitive. To succeed in this industry, it’s important to understand the different distribution channels that are available, such as physical stores and online platforms. For example, Under Armour is a well-known apparel business that sells its products through both physical and digital channels.

As you begin your active investment journey, it’s important to learn as much as you can about the company you are interested in. This includes understanding its products, management, and business risks. It’s also a good idea to ask critical questions and do your own research to ensure that you have confidence in your investment. Remember to start with the basics and learn about the company before diving into financial statements, as this will help you to better understand the financial results. Overall, the key is to find the perfect ingredients for a successful investment by doing thorough research and asking the right questions.

Here are some initial questions I might ask about Under Armour:

Why is Under Amour (UA) a better investment than its competitors?

What makes UA better than other apparel businesses?

Does UA have any patents on their clothes and shoes?

Who manufactures UA clothes?

Is there a contract or partnership from the manufacturer?

Why was this manufacturer selected?

Who are UA shipping partners?

Is UA shipping partner contract?

Does UA have its own stores? Why does UA have its own stores?

How many stores does UA have?

How many retail partnerships do they have?

Did Under Armour ship their apparel from a warehouse, and from which warehouse?

How did UA decide to pick this warehouse?

Where were the clothes made?

Who designs UA’s clothes?

What is the designing strategy, do they create athleisure clothes or not?

Who’s the design team leader, how long did they work at the firm? Do they have experience at other firms?

Notice that I did not list any financial or math-related questions. The point of this exercise is to get familiar with the industry and business. As you are learning, there will be more financial jargon and it will get more confusing. Do not be discouraged. If it is confusing, you are learning.

3. Learn about investment strategies (Week 3)

There are many investment strategies to choose from, but one that has proven to be effective in achieving above-average market returns is value investing. This strategy involves identifying undervalued companies and investing in them with the expectation that their value will increase over time.

Value investing has been used successfully by many billionaire investors, including Warren Buffet, Seth Klarman, and Bill Ackman. It is considered a solid foundation for investors to learn about other investment strategies and can be a powerful tool for building long-term wealth. If you are new to investing, learning about value investing and how to apply it to your portfolio can be a valuable way to start building your investment strategy.

What exactly is value investing?

Value investing identifies companies with a current market price that is less than their intrinsic worth, which means the stock or company is “undervalued.”

How do I determine the value of a stock and know if a stock is undervalued?

The discounted cash flow – this method provides the net present value by estimating the company’s future profitability to help determine the company’s values. The discounted cash flow will help provide a range of value to the entire business.

Another way to find undervalued stocks is by using the valuation ratio. A valuation ratio shows the relationship between a company’s market value or its equity and some fundamental financial metric (e.g., earnings). The point of a valuation ratio shows the price you pay for some stream of earnings, revenue, or cash flow (or other financial metrics).

Price/Earnings – The historical average of the S&P 500 index P/E is 15, therefore anything under 15 could be considered undervalued relative to the historical average of the S&P 500 index.

Price/Book – Price is the stock’s current market price. Book value represents what the total asset of the company is worth. So, if the price of a company is worth $100M, and the book value is worth $110M, you will see a P/B= .90 ($100M/$110M).

Not all undervalued stocks are suitable investments. Some companies may reflect undervalued but aren’t performant and stay that way. We call these value traps. A value trap will have a valuation that appears cheap, but it has risks and troubles that will cause the company to continue declining.

Understand why stocks become undervalued

Missed expectations and lower guidance: Shares can plunge if the company provides quarterly and annual reports that misses target earnings or provides guidance below Wall Street estimates.

Market crashes and corrections: If the entire market drops, it’s a great time to look for undervalued stocks.

Bad news: Just like when a stock misses an analysts’ expectations, bad news can cause a knee-jerk reaction from shareholders, sending shares plunging more than they should.

Cyclical fluctuations: Different sectors tend to perform better at different stages of the economic cycle, and it can be useful to look for bargains in industries that are currently out of favor. However, it’s important to remember that not all out of favor sectors will recover or return to normal business operations. For example, the restaurant and retail industries are both known for having a high rate of businesses that go out of business.

Value investing involves looking for undervalued stocks that have the potential to increase in value over time. For example, Tesla stock priced at $200 could be considered a value stock if investors are underestimating the technology and complexity of the company, just as investors initially underestimated the software, ecosystem, and design of the iPhone when it was first released. The general concept behind value investing is to look for opportunities to buy undervalued stocks at a discounted price, similar to buying a $100 bill for $70. While value investing is a straightforward concept, it can be challenging to master, as it requires careful analysis and research to identify undervalued stocks that are right for your portfolio.

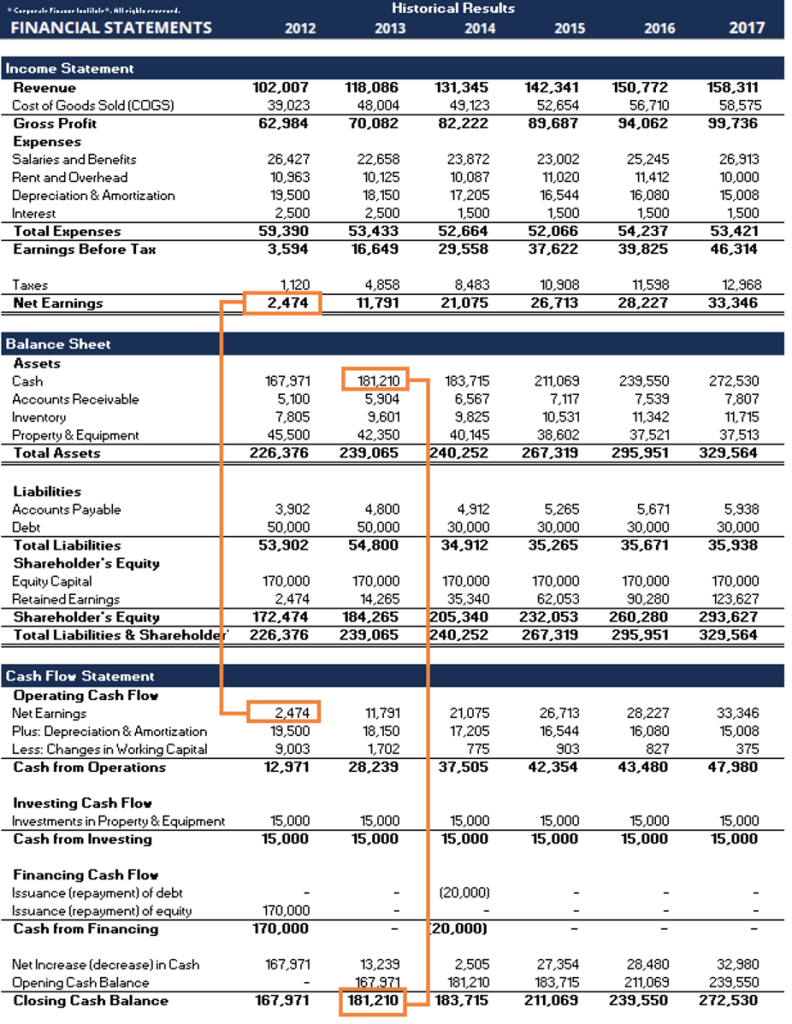

4. Learn how to read financial statements and how to create one from scratch (Week 4)

Financial statements will be disconcerting to learn. If math isn’t one of your strongest skills, it will be considerably more difficult. But, most of the investment math is simple algebra. If you cannot interpret a financial statement well, don’t rush to buy stocks. Start a stock account or paper trading account with only the amount that you can afford to lose, but still assert the same spending habits that you would with a larger account. The amount of money you need to buy an individual stock depends on your investment experience and skills.

How do you know when you are fundamentally ready to invest?

Q: Can you identify seasonality in a financial statement?

Q: What happens to cash flow if customers are paying with credit cards instead of cash?

Q: How much profit does a company have to pay off its current debt obligations?

Q: Can you teach someone how to read a financial statement

As millennials and Gen Z enter the workforce, it’s important to adopt a frugal mindset in order to manage finances effectively to live the ‘Frugalpreneur’ lifestyle, keeping the largest expenses as low as possible. Many successful entrepreneurs have kept their expenses low in order to finance their businesses, and by adopting this mindset you can achieve financial success. It is important to make smart financial choices and avoid purchases that don’t add value to your life.

There are many overpriced “brand activities” in a society that put pressure on millennials and impose expensive social obligations on them. Social branding activities such as weddings, cars, luxury goods, independent living, travel and many others are responsible for Millennials’ financial stress. Who would you like to impress? In fact, most of these branding tactics are just ways for companies to make money, they usually do not add value to your life. If you can afford the social brand image, do it wisely, but don’t go into debt.

The average salary of millennials ranges from $60,000 to $100,000 per year. HENRY (High Earners Not Rich, Still) Millennials make $100,000 or more. Saving and investing in your early career might not look like much, but just wait until you reach your 30s. Millennials and Gen Zs, listen to me if you want a better financial life: your priorities must change. Money cannot solve personal life problems, but financial flexibility can relieve some of life’s difficulties. Utilize your money for purchases that will add the greatest value to your life at the best price. Living an intelligent financial lifestyle doesn’t look sexy because society is driven by marketing your life into perpetual spending habits with overrated experiences, temporary homes, and worthless cars.

Living independent – Very Overrated

Living independently can be a very overrated concept, and there are several reasons for this. One of the most straightforward ways to save money is to live with your parents or have a roommate. Rent is typically one of the highest recurring expenses, so cutting down on it can make a significant impact on your budget.

Society may often put pressure on millennials to live independently, but living with your family or having roommates can actually be a sign of maturity and good financial decision-making. Even if you are making a good income, it may still be more cost-effective to live at home or with a roommate rather than paying for an expensive apartment on your own. Unless there are specific issues at home, living with your family can be a smart financial decision that can help you save money.

Many millennials feel pressure to live independently and may go into debt in order to impress others with their financial status. However, these types of expenses, such as renting an apartment or buying a new car, do not necessarily add value to one’s life beyond the illusion of financial success.

A colleague of mine, Kevin, once asked me how I could afford to eat out for lunch every day. Kevin had lived with roommates for two years before renting a one-bedroom apartment in Arlington, VA for $2,300 per month. It’s worth considering whether the expense of living independently is worth it, and whether it’s possible to make more financially sound decisions that can benefit your long-term financial health.

Kevin’s background: Kevin lived with roommates for two years, and then rented his own one-bedroom apartment in Arlington, VA for $2,300 a month.

Kevin: “Tom you are wasting a lot of money eating out.”

Tom: “How much are you saving from not eating out?”

Kevin: “$200 a month” and he showed a big smile.

Tom: “Wow that’s great, but I like eating out. I am sacrificing my personal space to live with roommates.”

Kevin: “Oh you’re saving a lot of money living with roommates, I can’t do that though. I want my own space.”

Tom: “Yep, I am saving a lot of money,” I flashed a big smile back to Kevin and went out to lunch.

How much was I saving from living with roommates?

$0 Dollars – I never had to pay any rent.

During college and my first two years on the job, I paid $600 a month to live with my family. I saved much of my money in order to eventually buy a house. After saving up for a deposit, I was able to purchase a townhouse near a university campus. My mortgage was $2000 a month and my homeowners association (HOA) fees were $100 per month. I wasted no time in posting available rooms for rent. I lived on my own for less than a month before I had a college roommate who moved into my house. Within the second month, all the rooms were rented. There were times when I rented out my own bedroom on Airbnb and slept on the sofa. This may seem extreme, but it helped me save money more quickly.

While some people have had bad experiences living with roommates, it is understandable that it may not always be convenient. It takes time to interview potential roommates and ensure they have good etiquette.

I am not saying that millennials have to live with their families, but who do they want to impress? You can always live independently with your family by paying rent and helping to care for the home. If living with family is not a viable option, then look for a good roommate.

If you want to live independently, consider renting an affordable basement and sharing a kitchen. Whatever you do, try to minimize your rental expenses as much as possible. Saving money on things like coffee, eating out, and being frugal with other smaller discretionary expenses does not compare to saving money on rental expenses.

Traveling often – Overrated

Traveling is great, but why are millennials traveling so often? There should be a budget set for traveling. I am worried about my generation that is taking out loans and paying interest to travel more often. Does traveling often add value to anyone’s life? It could, but at what cost?

Eating out – Underrated

I can’t eat simple prepared meals like sandwiches, pizza, etc. I prefer meals that have a richer taste, which means they take longer to cook. I have to spend a lot of time grocery shopping, preparing, and cleaning just to make one meal. To me, it’s not worth the time to cook unless I’m cooking for a household of at least three people. The economic cost and time required to prepare a meal are wasteful. It would be just as affordable, and sometimes cheaper, to eat out than to make the food at home.

10% minimal saving & 10% Retirement – Very Underrated

It is important to pay off your discretionary debt that has an interest rate above 5%. This includes paying off your credit card balances in full each month. There is no reason to carry a balance from month to month.

Once you have paid off your credit card debt, it is a good idea to start saving 10% of your income each month. However, it is not advisable to simply leave your savings in a regular savings account. Instead, consider investing your savings in a higher-yielding account, such as a stock market index fund. Avoid picking individual stocks unless you are well-educated in investment fundamentals, such as reading financial statements and understanding financial risks.

It is always a good idea to invest in your retirement, even if you are self-employed or work as a freelancer. The average employer match is 3%, so you would need to contribute 6% of your income to receive the additional 3% from your employer. If you are self-employed, it is recommended to invest at least 10% of your income in your retirement.

Buy a used, Affordable Car – Very Underrated

It’s understandable that you want to impress others, but the reality is that financial stability is more important than the material possessions you own. Buying a used, affordable car is often underrated and a wiser financial decision than purchasing a new, expensive one. The only people who will be impressed by the beautiful cars are hidden fees that will treat you like a financial resource for their entertainment.

Expensive Wedding and Wedding Rings – Overrated

Weddings and wedding rings can also be overrated, as the average cost of a wedding in the United States is over $20,000. It’s not worth taking out a loan or delaying important financial goals, such as purchasing a home, just to have an extravagant wedding.

In many Asian cultures, cash gifts are a common part of wedding celebrations and can help offset some of the costs. While it’s understandable to want to have a memorable wedding experience and express gratitude to family and friends, it’s important to consider your financial situation and budget accordingly.

If you have the means to have an expensive wedding without impacting your ability to achieve financial goals, then go ahead. However, if it means delaying your ability to buy a home or causing financial strain, it’s important to prioritize those financial goals over a lavish wedding.

Birthday Gifts and Christmas Gifts – overrated

We should not be shopping for random gifts. If you need to buy a gift for a special occasion, make sure it is useful. Often, we purchase poor gifts or try to give frivolous gifts that end up being sold at a garage sale or donated. Instead, consider paying for an event, a meal, or something that will help maintain a good relationship with the person you are giving the gift to.

Fast Fashion and Cheap Fashion – overrated

It’s important to focus on quality when shopping for clothes and accessories. Fast fashion items are often of low quality, and it’s better to invest in higher quality items that may cost a bit more. This way, you’ll have fewer low-quality items cluttering up your closet.

For example, consider investing in dress shoes, suits, and purses that are made with quality materials. While some brands, like Louis Vuitton, offer entry-level luxury items that may not be as well-made as others in the same price range, it’s worth considering investing in a brand like Hermes, whose items often have a higher resale value.

It’s important to also be mindful of the quality of items within a certain price range. For example, Michael Kors bags that cost $300 may not be as high quality as other options in the same price range, which could be a contributing factor to the brand’s declining brand equity. Investing in quality items is a smart choice that will pay off in the long run.

Used Electronics – Underrated

As a savvy shopper, I prefer to purchase used electronics rather than shelling out for brand new ones. Not only do I save money by buying second hand, but I also have the opportunity to find high-quality products at a fraction of their original cost.

When shopping for electronics, it’s important to consider the capabilities of the product rather than simply going for the latest and greatest model. Many older electronics, especially those that are just a generation or two behind, are still more than capable of performing at a high level and meeting your needs.

Plus, buying used electronics is an environmentally friendly choice. It helps to reduce waste and keep these products out of landfills, while also supporting the circular economy.

So next time you’re in the market for electronics, consider opting for a gently used option. You’ll save money and feel good about your purchase, all while getting the performance you need.