We stand at a unique economic juncture. For years, conflicting signals often muddied the waters, creating a confusing landscape: strong employment masked weak demand, loose credit existed despite slowing growth, and dovish policy battled rising inflation. These contradictions weren’t just noise; they acted as buffers, often delaying inevitable corrections.

Today, that buffer seems gone. The major risk indicators I track encompass a wide range. They include leading indicators like yield curve inversions and manufacturing PMIs. They also cover credit market stress. Even lagging indicators like employment are now showing cracks. All these indicators are finally pointing in the same direction. This synchronized alignment is what truly concerns me, and it prompts questions I often hear: “Are you ever optimistic? Has it just been doom and gloom for 15 years? Do you even invest, and have you beaten the S&P?”

These are fair questions, especially given my recent cautious tone. My current stance isn’t about predicting doomsday; it’s about recognizing a rare confluence of macroeconomic risks demanding a different approach. And no, I haven’t always been bearish.

(Note: A detailed breakdown of those specific economic signals is in my related Thread post — this blog focuses on the ‘why’ behind my perspective.)

My Investment Pivot: From 2009 Bull to 2021 Pause

For the vast majority of my investment journey, particularly from the market ashes of 2009 through late 2021, I was aggressively bullish. I actively rode one of the most powerful bull markets in modern history. I rotated through sectors and captured significant gains in growth stocks. Yes, I cumulatively beat the S&P 500 benchmark over that extended period. While not every single year was an outperformer, the long-term strategy delivered.

My decision to significantly reduce exposure in December 2021 was driven by two factors. The first was the practical need for liquidity as I was starting a new business venture. The second was a growing unease with stretched market valuations. While timing often involves luck, this move significantly shielded me from the worst of the 2022 drawdown.

The pandemic era became a turning point in my analysis. It prompted a deeper dive into macroeconomics – exploring the mechanics of debt cycles, the true power (and limitations) of monetary policy, and the complex dynamics of inflation. Watching the unprecedented global response, the massive fiscal injections, and the subsequent inflationary pressures made theoretical concepts starkly real.

I began to appreciate the inherent fragility within the economic system when pushed to extremes. Figures like Ray Dalio, whose warnings about debt spirals once seemed abstract, suddenly felt prescient. It also highlighted how quickly conventional wisdom can be overturned. I saw Michael Burry struggle with his 2023 short attempt, then pivot to undervalued Chinese equities like $BABA (which I also briefly traded in the $80s). This reinforced a key lesson: valuation isn’t everything. Overlooked geopolitical and policy risks can dominate fundamentals. This evolving global picture ultimately led me to exit even long-term holdings I previously favored.

• Mid 2022 Onward: Tactical Precision Over Board Optimism: Re-entering the market mid-2022 wasn’t a return to broad bullishness. It was about targeted, tactical trades where risk/reward seemed skewed in my favor. This involved:

• Selective Shorts: Targeting names showing technical breakdowns and appearing fundamentally overextended, like $TSLA, $BYND, and $SFIX.

• Contrarian Longs: Building a significant position in $META. Despite the negative sentiment, its core business strength compared to its valuation seemed deeply misunderstood. I held through the painful drawdown into late 2022/early 2023, even adding significantly to my position. I began scaling out of $META as it recovered strongly through Dec 2024. I eventually exited most of the position around the $600 level in late 2024 or early 2025. The highly speculative assets surge again despite clear signals the Fed wasn’t easing, suggesting market froth was outweighing fundamentals.

• Conviction Play: My focus shifted to $CELH, a company I’d followed since 2018 (initially alongside $REED). I saw $CELH as having tremendous potential over the next 5-10 years. I built a position through 2023 and exited entirely after a significant run-up concluded around February 2025. That marked the end of my last major long equity position.

Macro Warnings and the Challenge of Timing from Others

Many smart investors like Druckenmiller, Burry, and Dalio started sounding alarms years ago. They identified significant structural risks that were, and still are, valid concerns. However, their experiences highlight the brutal challenge of timing the market, even when your thesis is fundamentally sound.

Let’s look at their calls:

Stanley Druckenmiller’s Warnings:

In 2022, Druckenmiller warned of a potential “lost decade” for equities, predicting that U.S. stocks could deliver flat or minimal returns over the next 10 years. He attributed this outlook to several macroeconomic shifts, including:

• Persistent inflation

• Rising interest rates

• Deglobalization

• The end of easy monetary policy

“We’ve had a tsunami of money since 2009. All of that is going away.”

— Druckenmiller, Delivering Alpha 2022

Druckenmiller argued the bull run was built on unsustainable tailwinds — and those are now reversing. He emphasized that the favorable conditions supporting the previous bull market were reversing. These conditions, such as low interest rates and globalization, led to a more challenging investment environment. By 2023, his concern deepened. Speaking at the Sohn Conference, he called U.S. fiscal policy a “horror movie” and warned:

“If current trends continue, we could see a fiscal crisis by 2030.”

• Debt interest could soon exceed defense spending

• No political will to address structural deficits

• Rising risk of a bond market event

Additionally, he cautioned that the Federal Reserve might have declared victory over inflation prematurely. He was concerned that cutting interest rates during a strong economy could cause inflation to resurge. This situation draws parallels to the economic patterns of the 1970s.

Michael Burry $1.6 Billion Short Attempt:

Michael Burry—the legendary investor behind “The Big Short” made headlines again in 2023. But this time, it wasn’t for calling a housing crash. It was for betting big against the broader U.S. stock market. In mid-2023, Burry’s hedge fund, Scion Asset Management, disclosed large short positions. These were through put options on two major index ETFs:

• SPDR S&P 500 ETF (SPY)

• Invesco QQQ Trust (QQQ)

The combined notional value of these positions totaled $1.6 billion. While headlines focused on the size, it’s important to clarify: that figure represents the exposure. It is not the actual capital at risk. The premiums paid on options are much lower. Still, it was a bold and aggressive stance.

Why Burry Went Bearish:

Burry laid out his macro concerns clearly across interviews and social media:

Inflation would return: In early 2023, he wrote, “Inflation peaked. But it is not the last peak of this cycle… and the US in recession by any definition.”

• Recession Risk: He believed the U.S. economy was entering a slowdown masked by lagging data.

• Overstretched Valuations: Burry saw the tech rally—particularly in the Nasdaq-100 as reminiscent of previous market bubbles.

• Passive Investing Bubble: He’s been warning since 2019 that passive index flows distort market signals and create dangerous concentration in large-cap names.

To Burry, all of this added up to one conclusion: stocks were headed for a fall.

What Happened Next:

Unfortunately for Burry, markets had other plans. By the third quarter of 2023, both the S&P 500 and Nasdaq-100 had rallied sharply. The AI boom and renewed bullish sentiment powered tech stocks, undermining Burry’s thesis—at least in the short term. According to reports, Scion closed the short positions, and some analysts estimate the fund took a loss of around 40% on the trade.

The Semiconductor Shift:

After closing his broader market shorts, Burry didn’t sit still. He turned his bearish sights on another sector: semiconductors. Through new put options on the iShares Semiconductor ETF ($SOXX), Burry bet against a sector riding high on AI optimism. Yet again, the timing was rough—Nvidia and other chipmakers continued to surge, fueled by strong demand and investor enthusiasm.

Ray Dalio’s Structural Warnings:

Ray Dalio offers a similar lesson in macro-based caution. He’s been sounding alarms about market fragility for years, pointing to prolonged ultra-low interest rates and historical levels of quantitative easing. Like Burry and Druckenmiller, Dalio saw the structural risks inherent in the system. But unlike Burry, he didn’t place massive short bets trying to time a collapse. Still, his belief in powerful macro headwinds was strong. This conviction influenced Bridgewater’s positioning and led to underperformance at a time when markets were fueled more by liquidity and policy than traditional logic.

The Takeaway: Timing vs. Thesis

In theory, these elite macro investors were fundamentally right about many of the underlying risks: valuations were stretched, debt levels were unsustainable, productivity was slowing.

But timing matters immensely.

The primary reason their “doomsday” scenarios were early was due to unprecedented policy responses. In 2018, the Fed tried to hike and normalize policy, but the market panicked, and Powell backed off in 2019. Then COVID hit, and the U.S. injected $5 trillion in stimulus, rates were cut to zero, and the Fed ran historic QE. It wasn’t just stimulus; it was a liquidity shockwave. Every asset surged: crypto, meme stocks, tech, housing. Years of growth were pulled forward. The crash wasn’t canceled; it was delayed, kicked down the road by artificial means.

This is why Burry’s concerns in 2023, while valid, weren’t what the market was pricing in. Markets don’t move on fundamentals alone. They move on liquidity, positioning, and narrative momentum. In 2023, those forces drowned out macro caution, and Burry’s thesis got buried in the noise. His short became a textbook example of one of investing’s most brutal lessons: being early can still mean being wrong, even if you’re fundamentally right. Consider Warren Buffett in 1999, who warned about dot-coms being untethered from reality, yet the Nasdaq rallied another 80% before crashing. Buffett sat in cash; Burry tried to time the top.

Ironically, I think Burry is making another major misstep now by going long on China in this environment. He seems to believe China will be insulated from global risk, but I see it differently: U.S. market risk is global risk, and no major economy is truly shielded from it.

Why It’s Different Now — And Much Closer

Today, we’re out of tools.

• The Fed can’t cut aggressively without reaccelerating inflation.

• It can’t hike without triggering a credit event.

• It’s boxed in.

The biggest underpriced risk is Debt servicing.

• Interest on U.S. debt is expected to exceed $1.7T/year soon — more than Medicare or defense.

• By 2026, it will eat up ~15% of the federal budget.

Congress has no easy fix:

• Default? Global depression.

• Raise taxes? Kills demand.

• Print? Destroys the currency.

• Yield curve suppression? That’s hoping for a soft landing in a storm.

This isn’t politics — it’s pure math. And it’s catching up fast.

Another overlooked warning sign is the banking sector

You’ll hear, “Banks are cheap—strong earnings, high liquidity, solid metrics.” And sure, on paper, that’s all true. But cheap valuations don’t happen by accident. They’re a signal.

Banks are being discounted for a reason:

• Hidden credit risk in commercial and consumer debt

• Unrealized losses from long-duration assets still on the books

• Off-balance-sheet derivative exposure

• Liquidity risks if higher-for-longer rates start to break something

Banks may look stable. However, they sit at the center of a fragile financial system. This system is more exposed than most people realize. If anything cracks, banks are the first domino and usually the last to fully recover.

The market isn’t ignoring banks. It’s avoiding them.

Investors prefer to chase the MAG7 and growth stories. They don’t do this because they’re cheap. They are the only things still producing returns in a distorted, risk-heavy environment.

Where I’m Positioned Now

I’m cautious and I hold:

• Cash (providing optionality)

• Gold (traditional hedge)

• Engaging in selective short term equity trades (income)

I’m not chasing AI or crypto. I am taking profits and understanding it’s important to underperform during this market. I hedge when appropriate. I’m not permanently out, I’m waiting for better odds.

Final Thoughts: Long-Term Bull, Short-Term Realist

I’ve been long the U.S. market far longer than I’ve been cautious. I still believe in American innovation, but belief doesn’t override math. Today’s market is pushing up against macro limits: rising debt costs, policy exhaustion, and cyclical pressures. Ignoring these signals isn’t optimism—it’s willful blindness to what’s coming.

Will this market grind higher? Absolutely. Liquidity and narrative can defy logic for extended periods. My experience navigating the COVID crash taught me that timing involves both analysis and luck. During the crash, I stayed invested anticipating government backstops. I pivoted bearish in late 2021. I also tactically traded the subsequent swings, including the AI wave via $PLTR, which I exited near the end of Feb 2025. It also taught me the importance of knowing when not to press your bets.

Timing isn’t always skill. Sometimes, it’s knowing when to stop pressing.

Final Thoughts: The Patience Afforded by a Profitable Cycle

Am I early in my caution? Maybe. But my perspective is shaped by how the last few years unfolded. Exiting near the 2021 peak locked in substantial gains from a historic bull run. I re-entered near the lows of 2022 and early 2023. This allowed me to capitalize on the unexpected strength of the AI-driven rally. That “double dip”, catching gains on both ends of the cycle—gives me a different vantage point. It also reinforces the one habit most investors never master: patience.

This isn’t new territory for me. After stepping out in late 2021, I waited six months before re-entering. I dollar-cost averaged on the way down, then got lucky when AI momentum kicked in earlier than expected. But that rally taught me something else, don’t overstay when risk and reward disconnect. I’m willing to step back again, for another year, and let the market recalibrate.

Once you’ve harvested meaningful profits, the need to squeeze every last point of upside fades. The priority shifts to protecting capital—especially when macro risks are no longer scattered but aligned. This isn’t about predicting a crash tomorrow. It’s about understanding the current risk/reward setup. It simply doesn’t warrant full exposure. This is particularly true for someone who’s already been through the full cycle.

That said, I’m not permanently sidelined. If job losses pile up, and the Fed faces political pressure to cut, the equation changes. This holds true even with inflation still elevated. I’d redeploy capital as real yields compress and policy shifts again. But any rally sparked by emergency cuts wouldn’t erase the deeper structural problems, it would just delay them.

That’s why I’m looking at long-dated puts. Not as a gamble, but as a defined-risk hedge in a market that refuses to price in fiscal reality.

I know a lot of retail investors are still recovering from the FOMO-driven missteps of 2021. Many bought into hype and DCA’d into broken narratives. Now that they’re finally back to breakeven or modest gains—they’re impatient, even defensive. Some get personal when I challenge the market’s sustainability.

Ironically, I was the one warning about the bubble in 2021. And now? We’re right back to those extremes. So no—I’m not re-entering at these levels. I’ll wait until we get closer to 4,000 on the S&P. I will also wait until government policy creates a new asymmetric setup. I can then lean into this setup. Successful investing isn’t about staying aggressive at all times. It’s about knowing when prudence trumps action.

I’ve done this before—exiting high, re-entering low, and walking away again when risks overwhelmed rewards. That discipline paid off. And once you’ve seen the power of patience, you’re never in a rush again.

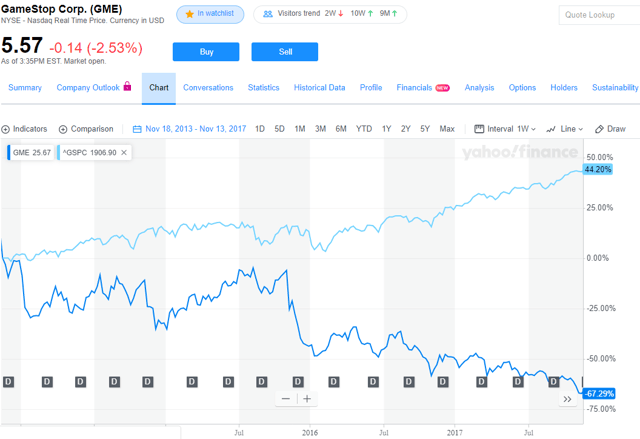

Playstation 4 was released on Nov 15, 2013. GME stock from Nov 2013 to Nov 2017 is -67%

Playstation 4 was released on Nov 15, 2013. GME stock from Nov 2013 to Nov 2017 is -67%