Why does the used video game industry exist? The rise and expansion of the used game stores such as GameStop (GME) in the 1990s to early 2000s.

Collectible video games, particularly those that are rare or used, became popular after baseball cards. The proliferation of internet technology also contributed to the growth of the used video game industry by allowing for the frequent production of video games and the creation of a robust secondary market for used games. Many customers were willing to trade their completed games for new or used ones due to the constant release of new game titles.

However, both the used video game and baseball card industries lack official marketplaces, leaving customers unsure of the fair price for what they are buying or selling.

(If you want to read more about Funoland history and how it became Gamestop go here: FuncoLand History: The Company Behind Used Video Games written by Ernie Smith)

As a teenager, I loved visiting FuncoLand, a used video game and technology store that ranked second on Forbes’ list of the fastest growing companies in 1998. FuncoLand was an excellent place to purchase both new and used video games, and it also had a few consoles available for customers to try out demos. In the early 2000s, FuncoLand merged with EB Games to become GameStop.

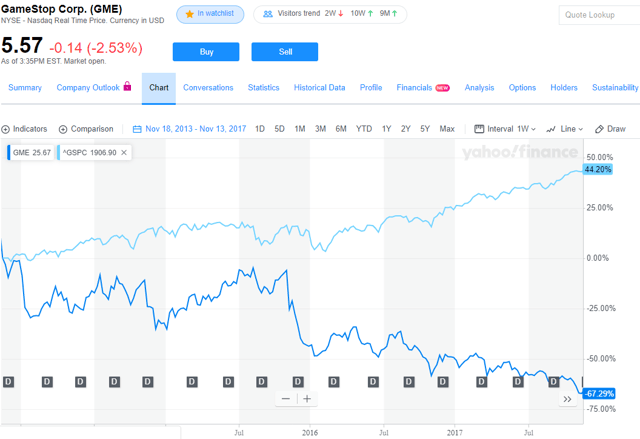

Reason #1: Since 2010, GameStop’s business model has been in decline due to a decrease in console unit sales, weak pricing power, the increasing popularity of digital downloads, and the decreasing value of used games. In the past decade, many retailers have struggled to survive, and even specialized private equity groups that have tried to revitalize the retail industry have ultimately failed. Many retail giants, such as Bonwit Tellers, Incredible Universe, and Kids “R” Us, have either disappeared or significantly downsized. Millennials may enjoy nostalgicically reminiscing about the 90s, but they are not likely to shop at GameStop due to its high prices, inconvenient locations, unethical business practices, and lack of authenticity. All niche communities are built on authenticity, and when GameStop changed its name and business model, it lost that authenticity as well.

Management has speculated that the release of new gaming consoles will help to boost sales in 2020. However, in the most recent quarter of 2019, GameStop’s CEO, George Sherman, was surprised by the steep decline in sales. There are now too many GameStop stores, and new and used games can be found much cheaper elsewhere. Some bullish investors believe that GameStop will automatically recover sales through the new gaming console cycle. However, over half of GameStop’s console market opportunities have vanished between 2008 and 2020. In 2008, a total of 90 million consoles were sold worldwide, while estimates for 2020 range from 30 to 40 million.

The Global Unit Sales of Current Generation Video Game Console in million units (2008 to 2017)Infogram.

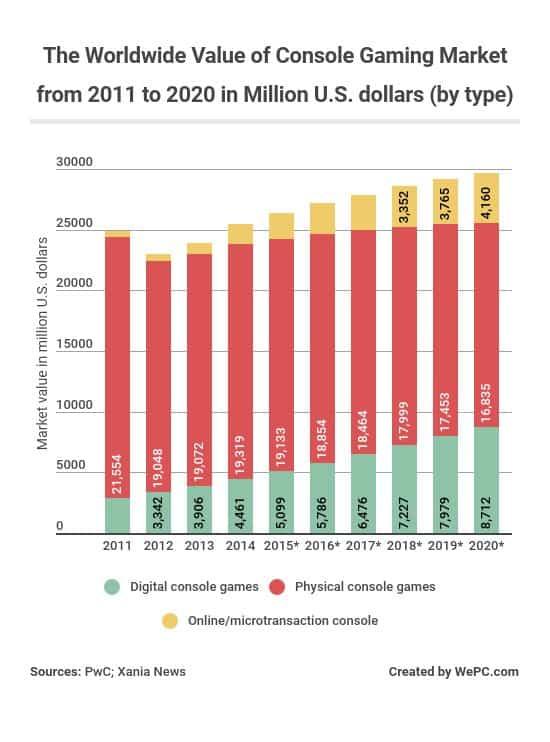

- Used games are becoming less valuable each year, while digital downloads are becoming more popular. Used games are still a significant source of income for GameStop, but its sales in that category have declined every year since 2011. In 2019, Sony sold over half of its games through downloads. Microsoft, Nintendo, and Google have all invested heavily in online gaming.

- GameStop’s supply chain and marketing tactics are some of the worst in the retail industry: They do not offer free shipping unless the total purchase is over $50, while their competitors are upgrading their businesses with robotics, software, and logistics innovations

- Corporate culture is toxic, and the business execution is mediocre: The gaming community is well aware of GameStop’s deceptive business practices. It is unclear what could make GameStop more successful than its competitors. In fact, it seems highly unlikely that the company’s management plan could result in success.

- Weak pricing power: New and popular games from other retailers are often discounted 10% less than Gamestop’s prices, and customers who use the retailers’ branded credit cards receive an additional 5% off. Additionally, used games can be found more cheaply on platforms such as eBay, Facebook, and Craigslist.

- GameStop cannot compete against cheaper alternatives: Major retailers are willing to take losses on gaming discounts in order to build brand loyalty and make up the difference with higher-margin products. GameStop has therefore resorted to offering creative membership deals that may mislead customers into paying more for used games.

- Used cheap games are recession-proof, not expensive used games: During a recession, consumers tend to look for the cheapest options rather than paying more for discretionary goods. Therefore, GameStop’s trade-in value may not make economic sense to many customers, as they can get a better value for their games through online retailers or platforms such as eBay, Facebook, or Craigslist. There are multiple ways to sell and buy games online that are more convenient and have considerably better prices. The cost of shipping video games is really affordable, and you will still make more money selling games on eBay than you would at GameStop.

- It’s not convenient to drive to a game store. Furthermore, it is more convenient for customers to buy games from larger retail stores where they can also purchase other items, rather than making a special trip to a game store. The supply of used video games is plentiful and it is easy to find popular titles from other marketplaces.

- Lack of Customer Service & Knowledge GameStop’s customer service and knowledge may also be lacking, as the company has unrealistic sales goals and uses forceful sales tactics. Its membership points system may also be confusing and misleading.

2. History of Poor Capital Allocation – Low ROIC, no investment in business and waste of share buybacks.

- Aggressive share buyback won’t work: GameStop’s aggressive share buyback strategy has been ineffective since 2010, costing the company over $400 million in share repurchases. This amount does not include the additional $120 million in buybacks from 2019. A company should only repurchase shares if it has sufficient funds to support its operations and the stock is selling at a significant discount to its calculated intrinsic value. However, GameStop is projected to run out of cash by the end of the year and will have to rely on high-interest credit to finance its operations.

- Liquidity Fallacy: The “liquidity fallacy” argument, which suggests that as long as customers continue to shop at GameStop, cash flow is not an issue, is flawed. While investor Michael Burry is well-versed in liquidity and cash flow, he and other investors failed to consider the cultural significance of the gaming community to GameStop’s business. Customers are the most important asset on GameStop’s balance sheet, not dollars. Just as Sears had enough liquidity to implement a turnaround strategy, but ultimately failed due to a lack of customer demand, cutting costs too deeply can negatively impact the customer experience and ultimately hurt the company’s financial performance.

- Fallen ROIC since 2014: Despite GameStop’s falling return on invested capital (ROIC) since 2014, due to a lack of significant investments in the business in recent years, Burry still identified it as one of his top investment ideas. It is unsurprising that investors may believe their skills and knowledge are transferable across industries, but in the constantly evolving world of gaming and retail, it is important to carefully assess all factors that could impact a company’s success.

3. Proposing unproven Strategies – gaming events, retro games, and merchandise will not replace the loss of used games revenue.

- Store gaming events are not proven strategies: Management has not provided information that shows gaming store events could create profitability. Most GameStop stores are simply too small for hosting gaming events. GameStop had a press release about their gaming events in Spring 2019, and it has been quiet ever since. GameStop probably has already failed its first gaming event attempt. The best gaming hosts in the industry are only mildly successful.

- Increasing retro and rare game sales will not stabilize revenue: Rare games sell on eBay at a much lower price than GameStop trade-in value. Collectible games will slow down the turnover inventory and they will take up shelf space from other, newer products.

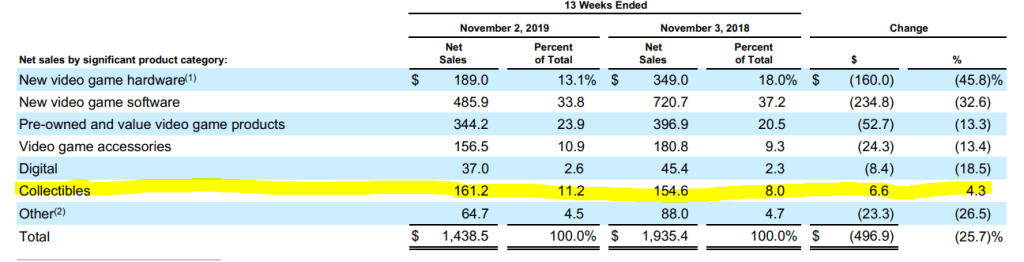

Shifting sales to nongaming merchandise will turn GameStop into another commodity store: GameStop owns the ThinkGeek store that sells nongaming merchandise and its sales are going down too. GameStop eliminated the position of Chief Operating Officer (COO) and in recent months has begun to switch some of its business models toward collectibles and trading merchandise. In other words, GameStop is basically converting its store into another failing business: its sister brand ThinkGeek. GameStop’s best non-selling items are Bubbleheads that are made by Funko. Gimmicky products like Bobbleheads are the beanie baby 2.0… Bobbleheads have high-net income margins, but it doesn’t add any value to GameStop. GameStop may get some foot traffic from Bobbleheads, socks, T-shirts, and other random merchandise, but total sales are simply not good enough to offset their declining game sales. In the early 90s, trading card stores attempted to switch from baseball cards to other popular merchandise, but eventually, the hobby store industry disappeared.

Gamestop is hoping for Collectibles to turnaround the company

Valuation Verdict:

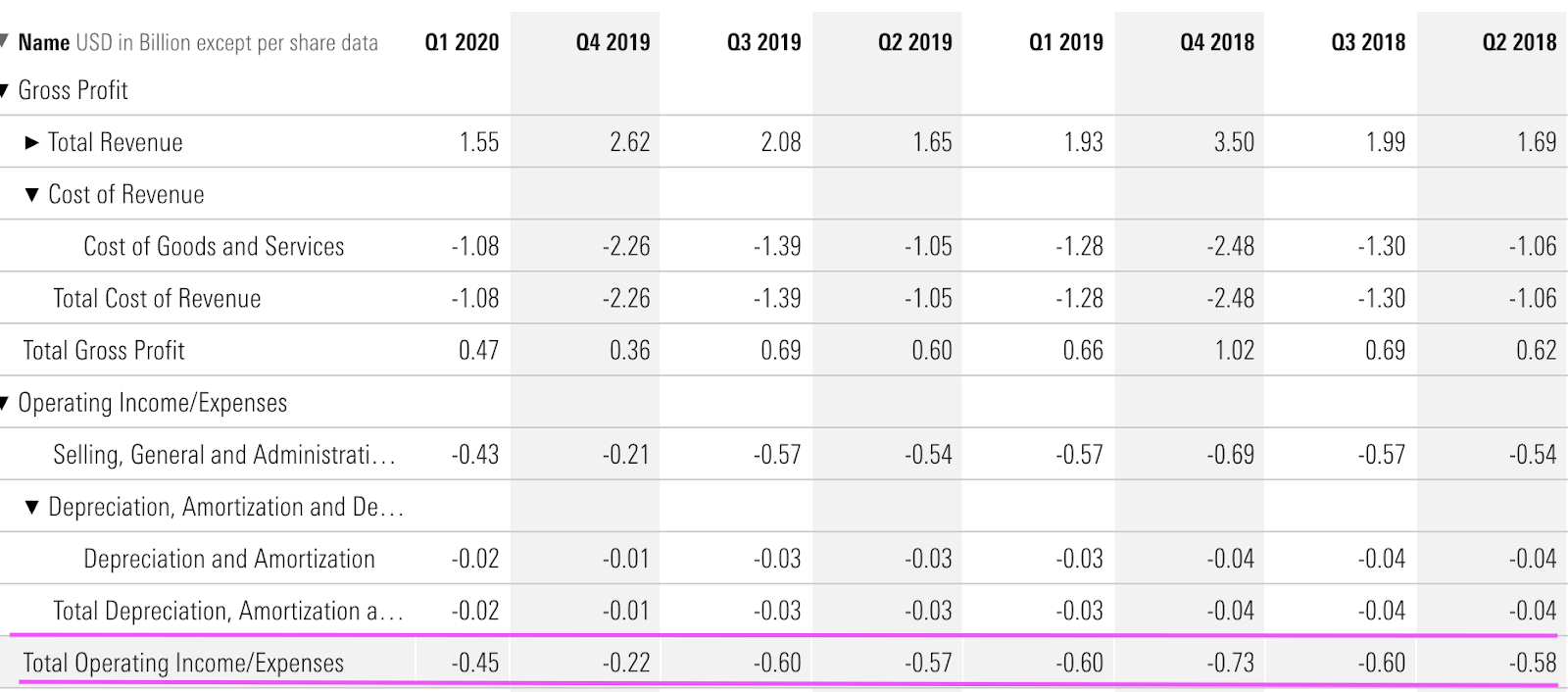

GME at its best would be worth $5/Share, assuming a small decline of -2% revenue CAGR and an average 3% EBITDA Margin. Bullish investors estimate GameStop valuation between $6 to $10, but it doesn’t require complex math to explain GameStop’s valuation. Analysts are overcompensating on complex valuation because they believe used video games can be a sustainable business model. The next 12 months will be critical for GameStop to improve its revenue or else the stock price will take a nose dive.

GameStop has less than one year to prove to investors that they can stabilize and improve sales. GameStop currently holds $290 million in cash and $419.4 million in debt. GameStop has had many years to turn around the company, but they have just burned through cash to buy back a company that offers customer zero value. Buybacks are great if the company is greatly undervalued and if it receives enough funds to support both business operations and buybacks. In GameStop’s case, it only has adequate money to pay down debt or buy back shares.

GME will drop to $3 again and become a penny stock in the next two years. Private Equity dry powder is at an all-time decade high, and there is still no offer for GameStop. Based on the last 4 quarters, GME is projected to lose a minimal of $160M to $200M in 2020.

Conclusion:

The existence of GameStop came from the void of the used game market. The industry has evolved and that used game void is available through multiple channels that offer cheaper prices and better value.

A new generation of game consoles is arriving later this year, buying GameStop sometime to hold out. The question remains, how much longer can GameStop’s business model remain relevant in a fast-growing digital distribution era? Get ready to say Rest In Peace, as GameStop will join its non-innovative retail family members in bankruptcy shortly.

Can’t stop, won’t stop, Gamestop selling drops ’cause it, it gets down baby, it gets down baby

The GameStop, gameflop, and StockDrop