It’s important to understand that there are two main approaches to investing in the stock market. The first is passive investing, which aims to achieve the average market return of around 7-8%.

The other approach is to invest in individual stocks with the goal of outperforming the S&P 500. This approach requires more time and effort, as it involves researching and selecting specific stocks rather than just investing in a broad index. If you have any specific questions or need clarification on anything mentioned in this post, feel free to reach out to me at TomNguyen@agarwoodcapital.com.

1. Decide if you want to put in the time to beat the stock market average returns (Week 1)

Passive investing- The goal of passive investing is to achieve average stock market returns, which are estimated to be around 7% to 8% over the last 100 years. To start passive investing, it is recommended to buy a mutual fund or ETF that represents the S&P 500. This can be done through robo-advisors or standard investment advisors, who provide these mutual funds and ETFs.

- When choosing a service for passive investing, it is important to go with low-cost options such as Vanguard or Fidelity, or robo-advisors like Wealthfront or Betterment. Management costs should be below 1% of your total asset value.

- A note about indexes: It is also important to note that different indexes represent different segments of the market. The S&P 500 represents the 500 largest companies in the US, and is therefore often used as a benchmark for the overall performance of the US stock market. Other indexes, such as the Dow Jones (DJI), only include a small number of companies and may not be representative of the broader market. This is why the S&P 500 is considered the standard benchmark instead of other indexes.

Active investing- The goal of active investing is to pick stocks and outperform the stock market average, which is represented by the S&P 500. Active investing requires putting in the time to research and analyze both individual stocks and the overall market. If you choose to become an active investor (or the DIY approach, as I like to call it), you will need to learn key aspects for analyzing a stock and strategies for ending the year with returns above the stock market average.

- Learning about an industry, company, and competitors

- Learning about investment strategies can outperform the average return

- Learning how to read and create financial statements

If becoming an active investor is the path you want, then continue reading.

2. Start by reading about industries and companies that are the most familiar to you. (Week 2)

It’s important to choose a business industry that is easy for you to comprehend, as this will make your investment journey more enjoyable and successful. One way to do this is to select an industry that is related to your profession or one that you have experience with through your regular purchases.

For example, if you work in the apparel industry, you may find it easier to understand the operations of an apparel company. The apparel industry is a multi-billion dollar investment opportunity, but it can also be highly competitive. To succeed in this industry, it’s important to understand the different distribution channels that are available, such as physical stores and online platforms. For example, Under Armour is a well-known apparel business that sells its products through both physical and digital channels.

As you begin your active investment journey, it’s important to learn as much as you can about the company you are interested in. This includes understanding its products, management, and business risks. It’s also a good idea to ask critical questions and do your own research to ensure that you have confidence in your investment. Remember to start with the basics and learn about the company before diving into financial statements, as this will help you to better understand the financial results. Overall, the key is to find the perfect ingredients for a successful investment by doing thorough research and asking the right questions.

Here are some initial questions I might ask about Under Armour:

- Why is Under Amour (UA) a better investment than its competitors?

- What makes UA better than other apparel businesses?

- Does UA have any patents on their clothes and shoes?

- Who manufactures UA clothes?

- Is there a contract or partnership from the manufacturer?

- Why was this manufacturer selected?

- Who are UA shipping partners?

- Is UA shipping partner contract?

- Does UA have its own stores? Why does UA have its own stores?

- How many stores does UA have?

- How many retail partnerships do they have?

- Did Under Armour ship their apparel from a warehouse, and from which warehouse?

- How did UA decide to pick this warehouse?

- Where were the clothes made?

- Who designs UA’s clothes?

- What is the designing strategy, do they create athleisure clothes or not?

- Who’s the design team leader, how long did they work at the firm? Do they have experience at other firms?

Notice that I did not list any financial or math-related questions. The point of this exercise is to get familiar with the industry and business. As you are learning, there will be more financial jargon and it will get more confusing. Do not be discouraged. If it is confusing, you are learning.

3. Learn about investment strategies (Week 3)

There are many investment strategies to choose from, but one that has proven to be effective in achieving above-average market returns is value investing. This strategy involves identifying undervalued companies and investing in them with the expectation that their value will increase over time.

Value investing has been used successfully by many billionaire investors, including Warren Buffet, Seth Klarman, and Bill Ackman. It is considered a solid foundation for investors to learn about other investment strategies and can be a powerful tool for building long-term wealth. If you are new to investing, learning about value investing and how to apply it to your portfolio can be a valuable way to start building your investment strategy.

What exactly is value investing?

Value investing identifies companies with a current market price that is less than their intrinsic worth, which means the stock or company is “undervalued.”

How do I determine the value of a stock and know if a stock is undervalued?

The discounted cash flow – this method provides the net present value by estimating the company’s future profitability to help determine the company’s values. The discounted cash flow will help provide a range of value to the entire business.

Another way to find undervalued stocks is by using the valuation ratio. A valuation ratio shows the relationship between a company’s market value or its equity and some fundamental financial metric (e.g., earnings). The point of a valuation ratio shows the price you pay for some stream of earnings, revenue, or cash flow (or other financial metrics).

- Price/Earnings – The historical average of the S&P 500 index P/E is 15, therefore anything under 15 could be considered undervalued relative to the historical average of the S&P 500 index.

- Price/Book – Price is the stock’s current market price. Book value represents what the total asset of the company is worth. So, if the price of a company is worth $100M, and the book value is worth $110M, you will see a P/B= .90 ($100M/$110M).

Not all undervalued stocks are suitable investments. Some companies may reflect undervalued but aren’t performant and stay that way. We call these value traps. A value trap will have a valuation that appears cheap, but it has risks and troubles that will cause the company to continue declining.

Understand why stocks become undervalued

- Missed expectations and lower guidance: Shares can plunge if the company provides quarterly and annual reports that misses target earnings or provides guidance below Wall Street estimates.

- Market crashes and corrections: If the entire market drops, it’s a great time to look for undervalued stocks.

- Bad news: Just like when a stock misses an analysts’ expectations, bad news can cause a knee-jerk reaction from shareholders, sending shares plunging more than they should.

Cyclical fluctuations: Different sectors tend to perform better at different stages of the economic cycle, and it can be useful to look for bargains in industries that are currently out of favor. However, it’s important to remember that not all out of favor sectors will recover or return to normal business operations. For example, the restaurant and retail industries are both known for having a high rate of businesses that go out of business.

Value investing involves looking for undervalued stocks that have the potential to increase in value over time. For example, Tesla stock priced at $200 could be considered a value stock if investors are underestimating the technology and complexity of the company, just as investors initially underestimated the software, ecosystem, and design of the iPhone when it was first released. The general concept behind value investing is to look for opportunities to buy undervalued stocks at a discounted price, similar to buying a $100 bill for $70. While value investing is a straightforward concept, it can be challenging to master, as it requires careful analysis and research to identify undervalued stocks that are right for your portfolio.

4. Learn how to read financial statements and how to create one from scratch (Week 4)

Financial statements will be disconcerting to learn. If math isn’t one of your strongest skills, it will be considerably more difficult. But, most of the investment math is simple algebra. If you cannot interpret a financial statement well, don’t rush to buy stocks. Start a stock account or paper trading account with only the amount that you can afford to lose, but still assert the same spending habits that you would with a larger account. The amount of money you need to buy an individual stock depends on your investment experience and skills.

How do you know when you are fundamentally ready to invest?

- Q: Can you identify seasonality in a financial statement?

- Q: What happens to cash flow if customers are paying with credit cards instead of cash?

- Q: How much profit does a company have to pay off its current debt obligations?

- Q: Can you teach someone how to read a financial statement

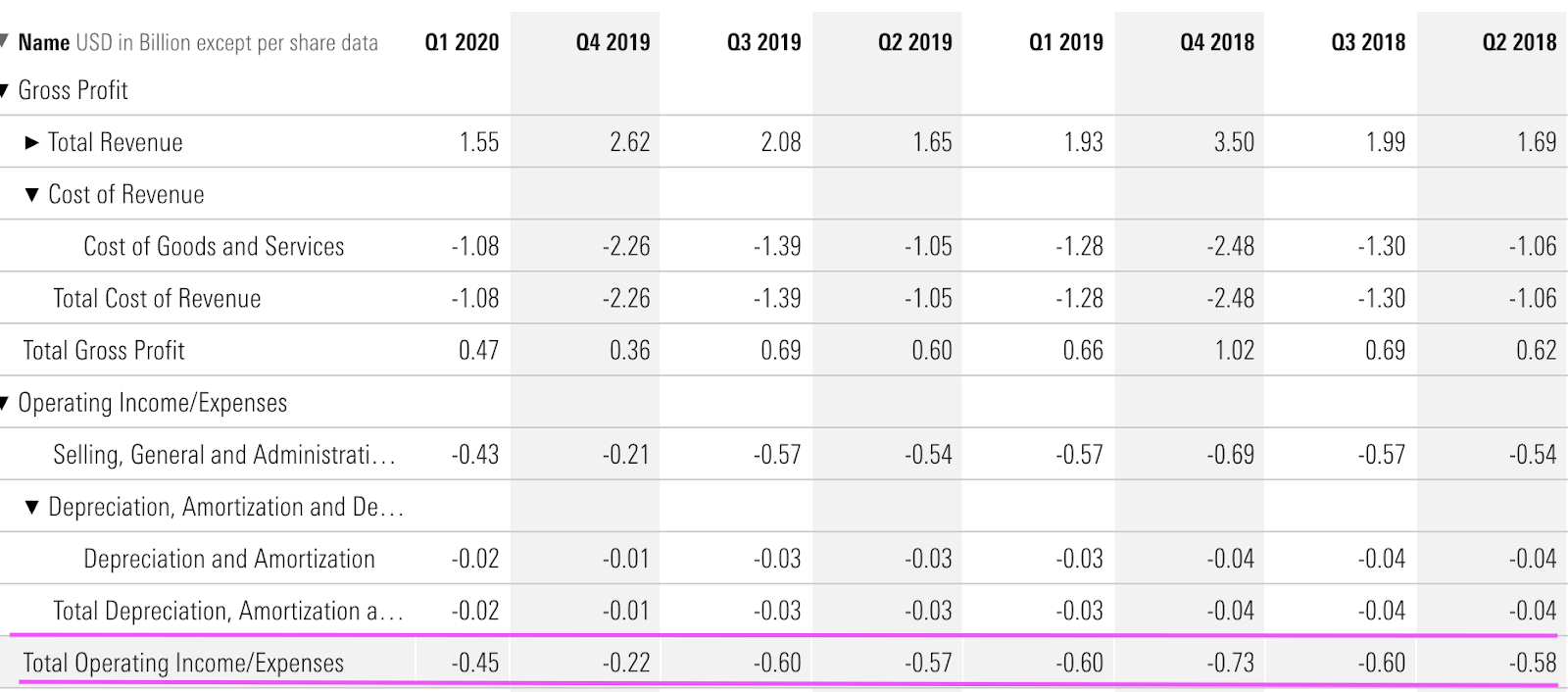

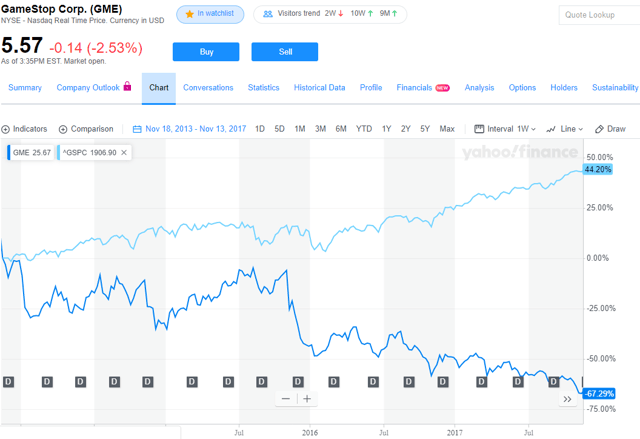

Playstation 4 was released on Nov 15, 2013. GME stock from Nov 2013 to Nov 2017 is -67%

Playstation 4 was released on Nov 15, 2013. GME stock from Nov 2013 to Nov 2017 is -67%